If you work in Software, there is a chance you are working at a company owned by a Private Equity (PE) firm. PE firms bought (invested) more than $400B worth of tech companies in 2021, doubling what they did in 2020. This accounted for 41% of $990B in overall PE deals done in 2021 as reported by WSJ.

With PE firms going into 2022 with $714B of dry power (capital available to spend) along with ambitions to raise even more capital in 2022, it would not be surprising to see the number of investments in Software double, meaning more PE ownership of Software companies in the market.

To understand the appeal of Software for PE investors, we need to first understand the rise of software.

The Rise of Software

Marc Andreessen famously penned the "Why Software Is Eating the World" article as a way to debunk the rise of another bubble back in 2011. Andreessen makes the case that this time around (in 2011), many of the prominent new Internet companies are building real, high-growth, high-margin, and highly defensible businesses. And since history is our greatest teacher, we can reflect back in 2022 and conclude that these new software companies have proven their worth over the last 11 years. They've built products that delighted their customers and established competitive advantages which have all gone towards justifying their rising valuations.

Silicon Valley invaded and overturned established industry structures in the last 10 years with expectations of many more industries to be disrupted in the future.

A common pattern for how established industries get disrupted is first using software and the internet as a channel for distribution (of existing products and services) and then moving into digital asset creation and delivery.

Amazon started by being a storefront where you bought physical books, shipped them to your house, to eventually selling digital assets (software powered eBooks, Kindle). Netflix started by being a storefront to order DVDs online and eventually moved into streaming digital assets (movies) directly to your devices.

Enter the Private Equity Investor

The past decade has seen many successful Software company IPOs which helped drive private market valuations along the way. These IPOs showed that the market valued software companies at higher multiples (P/E ratios) while demonstrating that mature subscription-based software companies generated healthy EBITDA and cash flows.

When there is value on the table, there is always someone around to capture it. Enter the Private Equity Investor. As the name suggests, private money is raised from individual investors and institutions which is then used to buy up equity (software companies) today with expectations of selling the equity at a higher multiple against future growth of revenue.

Private Equity firms had their start in mature industries like manufacturing, real estate, oil & gas, and financial services however within the last decade, the industry has embraced software because Software Companies have matured to become an Asset Class (maybe even commoditized), with a track record of generating returns that outperform other asset classes in the PE portfolio (link to Bain report). This has not only resulted in huge investments made into Software by existing PE firms but it has also made way for the rise of newer PE firms to service the smaller transaction segment in this space (Lower Middle Market).

PE Goals

There are typically 2 types of buyers for Software Companies. Investment firms, sometimes called financial sponsors (e.g. PE firms, Hedge Funds, Family Offices, Sovereign Wealth Fund) and strategics (other software/operating companies).

PE firms buy companies (assets) for one reason only. To generate a return for their investors. Their investment decisions are largely driven by financial models, factoring in other commercial, product, and technology opportunities and risks.

Contrast this to strategic buyers (other software/operating companies) whose analysis goes beyond the financial models (increased qualitative analysis) where they might be interested in an acquisition to further their product roadmap, enter a new market or even do an acqui-hire for talent.

Hence, financial sponsors can move fast in this market because their decisions are primarily based on the financial models and the quantitative aspects of the investment, when purchasing for the fund.

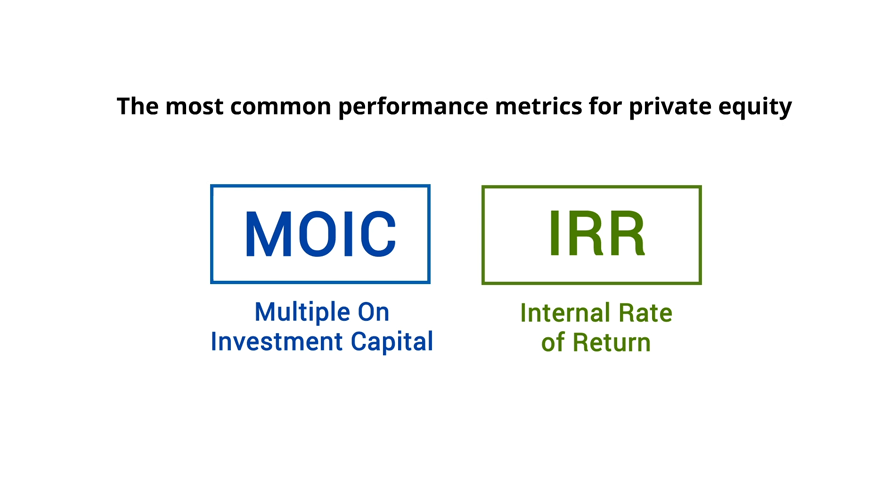

Two key metrics PE firms used to track their performance is IRR (Internal Rate of Return) and MOIC (Multiple on Invested Cash). IRR focuses on how much money is returned over a period of time while MOIC looks at how much money is generated from an investment (without the time component).

For simplicity sake, PE firms are looking to return anywhere from 3X to 6X MOIC. So for every $1MM invested, expect to generate between $3MM to $6MM of returns on invested capital. IRR can vary because a 3X return generated in 4 years will have a favorably IRR compared to the same 3X return generated in 7 years.

Software Economics

Over the last decade, Software has been the only asset class that can produce expected MOIC returns consistently due to the economics of software and the general uptrend of the industry.

Specifically enterprise software companies distributing software in a Software-As-A-Service (SaaS) model benefit from these 4 economic factors, making it a great asset class for investors.

Recurring Revenue

Enterprise software today is commonly sold on a recurring subscription model, referred to as Software-as-a-Service (SaaS), which provides for better predictability of revenue over a period of time. Customers that use business critical software this month will most likely continue to renew into the following month or year barring any critical issues with the software or service. This predictability of revenue (cash flow) is a great way to service debt (more on this later) which is a reason why PE firms love Software.

Gross Retention

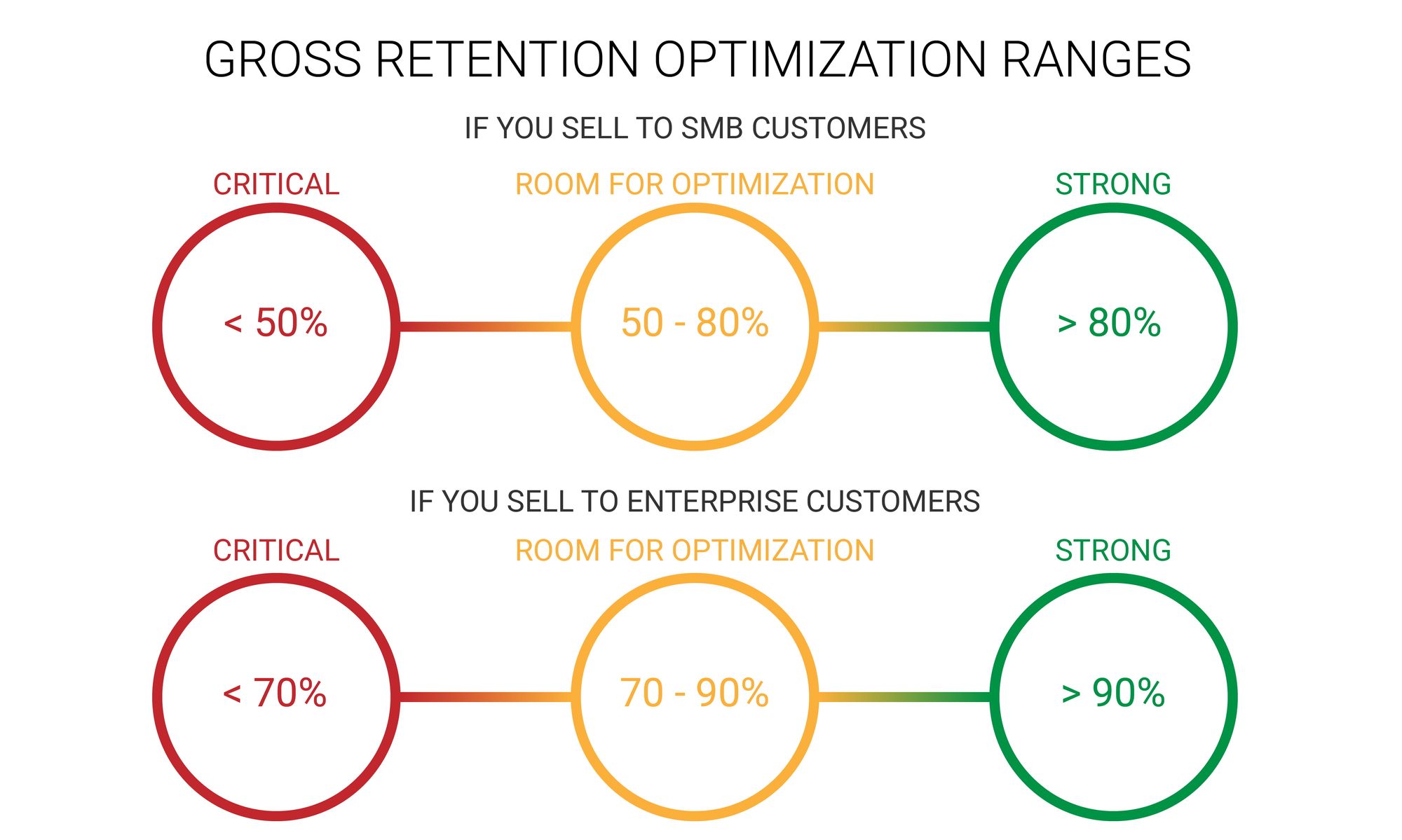

Another metric important in the SaaS world is Gross Retention. Gross retention captures the percentage of customers that return and subscribe to the service the following period (often measured yearly). An acceptable floor for this metric is ~80% gross retention. This means $1MM of revenue generated this year will result in $800K of revenue moving forward into the next year without any selling.

If your business is targeting a revenue growth rate of 40%, this implies that revenues have to be at $1.4MM. With Gross Retention at 80%, this means the business only needs to find $600K of additional revenue.

Let's stop and appreciate the importance of gross retention.

If you operated a non-subscription based business (e.g. other traditional industries), then growing 40% of revenues from last year means you start at ZERO and have to build up all $1.4MM of revenues for the following year. Compare that with the $600K you have to generate to realize a 40% growth in revenue.

The cost and effort to generate incremental 40% revenue growth is cheaper in Software, due to gross retention, compared to other industries, all things being equal.

Gross Margins

High gross margins is another metric that highlights why Software businesses are lucrative. High gross margins are a result of low COGS (cost of goods sold).

In a SaaS business, COGS includes:

- the cost of hosting (e.g. AWS),

- payments for software licenses,

- transactional costs (e.g. credit card processing fees)

- salaries for staff in support, customer success & training and onboarding teams

- salaries for staff maintaining your infrastructure

Companies that do a good job at managing COGS typically hover around 15% of revenue which results in a very high gross margin (85%) profile compared to other sectors. This is an important number as it dictates how much money you have left at the end of every month/year to fuel operating activities (Marketing, Finance, R&D) and most importantly, innovation and development of newer products to capture more of the market.

Marginal Cost

Another force multiplier in the Software business is that the marginal cost to service a new customer, if not zero, is very low compared to other industries. Software can be easily duplicated and shared across multiple customers, in real-time.

The more customers you serve, the lower the unit economics on COGS and the more value you capture on an ongoing basis (reselling the same asset over and over to extract as much value from it as possible).

All the profits are in the long-tail of the customer register, after the 1st customer.

If COGs can be stabilized to a percentage of revenue and operating expenses fixed, revenue from every incremental customer gain (or price increase) goes directly to the bottom line in the form of net profits.

Value Creation

Value Creation is the name of the game once a company is acquired by a PE firm. The clock starts ticking the day the deal is signed, rather than when the deal is closed (funded). The goal here is to exit the acquired company over the next 4 to 6 years with a 3X to 6X return on investment. If this can be done sooner, then the PE firm can boast better IRR metrics.

When you distill all the strategies and tactics PE firms have in their playbooks, there are only 2 real drivers to value creation.

Either grow the revenue or reduce expenses. Kudos if you can do both. Sounds pretty basic but every PE firm has their way (secret sauce) of driving to value.

Go-To-Market

A strong Go-To-Market (GTM) motion is often at the center of the value creation process as sales solves all problems (almost).

How you increase sales often has a trickle effect on the rest of the organization. Do you go up market, down market or move into adjacent markets? Do you focus on strengthening Gross Retention? Do you grow sales inorganically by acquiring other companies and building out a larger product portfolio?

The direction you need to take for Value Creation can often be found at the intersection of the Investment Thesis, Financial Models, and Commercial Due Diligence conducted by the PE firm during the investment process.

Talent

Another driver of value creation is assessing the current leadership to make a call on whether the existing team can propel the company forward as identified in the Investment Thesis and Financial Models.

Leadership is often assessed top down during diligence, starting from the C level and moving down to their direct reports, to ensure the presence of a strong team to guide the growth and scale of the organization over the next 5 years.

Product & Technology

The Go-To-Market strategies, leadership structure, and findings from diligence will often guide changes required within the Product and Technology functions. Alignment of the Products to support the Go-To-Market strategies along with the technology changes to support the Product, are critical in ensuring that the acquired companies achieves target financial projects for a successful exit.

Oftentimes, software companies will also find themselves having to raise their operational maturity, as a way to de-risk the investment for investors, to ensure operational excellence while also developing a strong and predictable approach to Product and Technology innovation to meet future goals.

Career Success under PE management

Given that Software is now a lucrative (and proven) asset class for investors, we will see more investments being made into software in 2022 and beyond.

Don't be surprised to find out that you might already be working at a software company owned by a PE firm today. The best way for you to be successful in this environment (and ownership) is to understand the Investment Thesis and Rationale for the purchase of your company. Talk to your manager or perhaps executive team and have them share the themes, direction and key strategic initiatives so that you can make better assumptions and drive actions aligned to the goals of the investor.

While your primary stakeholder was the Customer before a PE acquisition, you now have another key stakeholder, the PE investor, to account for in your strategies and tactical execution.

Learning how your PE firm operates, what drives their investment philosophies and how to take actions aligned to their goals could increase your career success going forward.